Equipment finance explained: lease vs loan vs chattel mortgage

- Finwave Finance

- Apr 20

- 7 min read

Key takeaways • Equipment finance is available for machinery, vehicles, technology, medical equipment, and more for businesses of all sizes. • The three main structures are finance lease, equipment loan (chattel mortgage), and commercial hire purchase. Each with different tax, ownership, and cash flow implications. • A finance lease lets you use the equipment without owning it, the lender owns the asset and you pay a monthly fee. • A chattel mortgage (equipment loan) transfers ownership to your business immediately - GST and depreciation benefits may apply. • Low-doc equipment finance is available for self-employed and ABN holders through Finwave's specialist lender panel. • A Finwave broker can help you identify which structure suits your business and access options across 80+ lenders. |

When your business needs a new piece of equipment, whether that's a vehicle, a machine, a fit-out, or a technology upgrade, how you finance it matters almost as much as what you buy. The structure you choose affects your cash flow, your tax position, and whether you own the asset at the end.

Most Australian small business owners are aware that equipment finance exists, but fewer understand the key differences between a finance lease, a standard equipment loan, and a chattel mortgage. This guide breaks down each structure clearly, including who each one is best suited to, so you can make an informed decision or have a more productive conversation with your broker.

Why equipment finance matters for small business in Australia

Paying cash for equipment ties up working capital that could be funding growth, covering wages, or managing seasonal cash flow gaps. Equipment finance lets businesses acquire the assets they need now and spread the cost over time preserving cash for the day-to-day.

Beyond cash flow, the right equipment finance structure can deliver meaningful tax advantages including GST credits, interest deductions, and depreciation claims. The wrong structure can mean missing out on those benefits or creating unexpected obligations at the end of the term.

What types of equipment can be financed? Finwave can help finance a wide range of business assets including: commercial vehicles and trucks, earthmoving and construction equipment, manufacturing machinery, medical and dental equipment, hospitality fit-outs, technology and IT infrastructure, agricultural equipment, and trailers and attachments. |

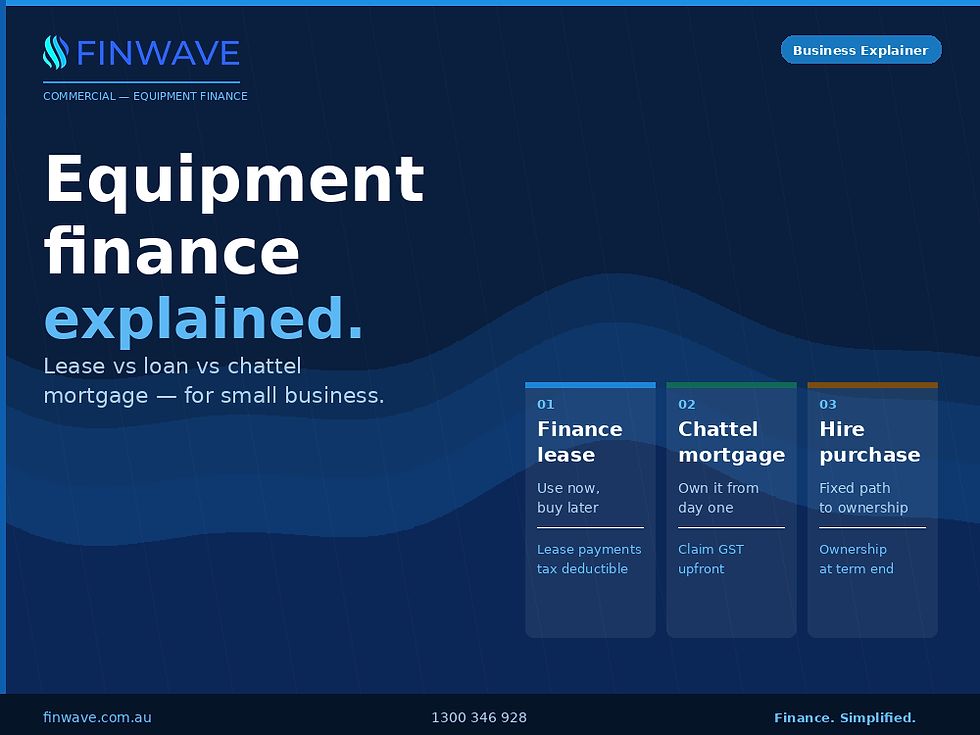

Option 1: finance lease

How it works

In a finance lease, the lender purchases the equipment and leases it to your business for an agreed term, typically 2 to 5 years. You make regular repayments during the lease period, and at the end of the term you have several options: return the equipment, extend the lease, or purchase the asset for its residual value.

Importantly, the lender retains ownership throughout the lease term. Your business has full use of the equipment but does not appear as the owner on the title.

Who it suits

• Businesses that want to keep the asset off the balance sheet

• Businesses that regularly upgrade equipment and want flexibility at the end of term

• Businesses that prefer lower monthly repayments (a residual reduces the repayment amount)

• Businesses where the equipment may be obsolete by the end of its useful life

Tax treatment

Lease repayments are generally 100% tax deductible as a business expense. However, because you don't own the asset, you cannot claim depreciation. GST on repayments may be claimable. Your accountant can confirm your specific position.

Always confirm tax treatment with your accountant. The information above is general in nature and individual circumstances vary. |

Option 2: chattel mortgage (equipment loan)

How it works

A chattel mortgage, also called an equipment loan is the most straightforward structure. Your business takes ownership of the equipment immediately, and the lender holds a mortgage (security interest) over the asset until the loan is repaid. Once you make the final payment, the mortgage is discharged and you own the asset outright.

Repayments are fixed over the loan term, giving you certainty in your cash flow planning. A balloon payment (residual) can be included at the end to reduce monthly repayments.

Who it suits

• Businesses that want to own the equipment immediately

• GST-registered businesses that can claim the full GST on purchase upfront

• Businesses looking to maximise depreciation benefits

• Businesses that plan to keep the equipment for the long term

• Self-employed borrowers, chattel mortgages are widely available on a low-doc basis

Tax treatment

As the owner of the asset from day one, your business can claim depreciation and the interest component of repayments as a tax deduction. GST-registered businesses can also claim the GST on the full purchase price upfront in the first BAS period, a significant cash flow advantage over a lease structure.

Option 3: commercial hire purchase

How it works

In a commercial hire purchase (CHP), the lender purchases the equipment and hires it to your business over an agreed term. You make regular repayments which cover both the principal and interest, and ownership transfers to your business automatically at the end of the term once all payments have been made. Unlike a finance lease, there is no option to return or walk away from the asset.

Who it suits

• Businesses that want to own the asset at the end but prefer a hire arrangement during the term

• Businesses that want fixed repayments with a clear path to ownership

• Businesses that cannot claim GST credits immediately (as GST is spread across repayments in a CHP)

Lease vs loan vs chattel mortgage: side-by-side comparison

| Finance lease | Chattel mortgage | Commercial hire purchase |

Ownership during term | Lender owns asset | Business owns immediately | Lender owns asset |

Ownership at end | Option to buy, return, or extend | Full ownership -mortgage discharged | Automatic transfer to business |

GST treatment | GST on repayments (claimable per BAS) | Full GST claimable upfront | GST spread across repayments |

Depreciation claim | No - lender claims depreciation | Yes - business claims depreciation | Yes - once owned at term end |

Interest deduction | Lease payments fully deductible | Interest component deductible | Interest component deductible |

Balance sheet | Asset off balance sheet | Asset on balance sheet | Asset on balance sheet |

Low-doc available | Yes | Yes - widely available | Yes |

Best for | Flexibility, regular upgrades | Ownership, GST-registered businesses | Fixed path to ownership |

Tax treatment is general guidance only The tax implications of each structure depend on your individual business circumstances, GST registration status, and applicable ATO rules at the time. Always confirm your position with a qualified accountant before choosing a structure. |

Which equipment finance structure is right for your business?

The right structure depends on three things: whether you want to own the equipment, how you want to treat it for tax purposes, and what your cash flow can support.

As a general starting point:

• Choose a chattel mortgage if you want immediate ownership, are GST-registered, and plan to keep the equipment long term

• Choose a finance lease if you want flexibility at the end of the term, prefer lower repayments, or regularly upgrade your equipment

• Choose a commercial hire purchase if you want a fixed path to ownership with no residual decision at the end

Your accountant can advise on the tax implications specific to your situation. A Finwave broker can then match you to the right lender and structure across a panel of 80+ lenders, including those who specialise in low-doc equipment finance for self-employed and ABN holders.

Equipment finance for self-employed and low-doc borrowers

If you're self-employed, a sole trader, or running a small business without two years of full financials, you may still be eligible for equipment finance through Finwave's lender panel. Many specialist lenders offer low-doc equipment finance, assessing applications on the basis of bank statements, BAS statements, or an accountant's letter rather than full tax returns.

Chattel mortgages in particular are widely available on a low-doc basis, especially where the loan is secured against the asset being purchased. ABN holders with at least 6 months of trading history are typically eligible to apply.

Frequently asked questions

Can I get equipment finance with bad credit?

Yes. Some lenders on Finwave's panel specialise in equipment finance for borrowers with imperfect credit histories. Approval and rates will depend on the specifics of your situation. Speak with a Finwave broker to understand what options may be available.

What is a balloon payment in equipment finance?

A balloon payment, also called a residual, is a lump sum payable at the end of the loan or lease term. By agreeing to pay a larger amount at the end, you reduce your regular repayments during the term. At the end, you can pay the balloon in cash, refinance it, or (in the case of a lease) use it as the purchase price if you choose to buy the asset.

How quickly can I get approved for equipment finance?

For standard applications, Finwave typically achieves approval within 24 to 48 hours. Some specialist lenders offer same-day approvals for eligible businesses. Having your asset details, ABN, and income evidence ready will speed the process significantly.

Can I finance used or second-hand equipment?

Yes. There is a strong second-hand market in Australia and most lenders will finance used equipment. Age, condition, and the existence of a clear title are key factors lenders assess. Finwave can advise on lender appetite for specific asset types and ages.

Get equipment finance through Finwave Whether you need a forklift, a truck, a fit-out, or a fleet of vehicles, Finwave compares 80+ lenders to find the right equipment finance structure for your business. Fast approvals, low-doc options available. Call 1300 346 928 | finwave.com.au/equipment-loans |

This article is general in nature and does not constitute financial or tax advice. Individual circumstances vary. Tax treatment of equipment finance structures depends on your business circumstances and applicable ATO rules — always consult a qualified accountant before choosing a finance structure. Please speak with a Finwave broker to discuss your specific situation. Finwave Finance Pty Ltd holds an Australian Credit Licence (ACL 561258).

Comments